1.0. INTRODUCTION

The use of digital technology and the internet is the source of disruption across sectors and is currently transforming various industries. Founders use big data analytics to understand market trends and consumer preferences to make more informed business decisions. Consumer access to smartphones and mobile internet has greatly increased the use of digital platforms across different sectors. Founders are relying on technology to provide solutions in building a global brand with continuous improvement in productivity, quality, agility, and service delivery.

We are currently in an era of smart, sustainable growth, and business entities are gearing towards solutions that would ease their processes and product & service delivery to consumers. Digital transformation has been immense. We experienced a surge during the pandemic, with a massive increase in the use of digital platforms, especially in the real estate sector.

The real estate sector is embracing technology-driven solutions to replace its old business infrastructure, processes, and strategies to create a more productive and predictable business model. Investors have seen the value of technology to the real estate sector, and it is unarguable that the digital disruption is creating a new future for the real estate industry. It is believed that investment in proptech would record over $ 50 billion worldwide by 2023.

Proptech is the future; it is changing how leading real estate firms manage their properties. We can streamline the importance of proptech into three main points;

Developing products and services that save time, and promote affordability.

Developing solutions that can mine external and internal data in near-real-time, and facilitate transparency.

Developing solutions that streamline operations from marketing and financial reporting to investment and property maintenance.

2.0. WHAT IS PROPTECH?

Proptech is an acronym for ‘property technology.’ It’s a term describing an ecosystem of startups offering technology-driven solutions across various aspects of commercial and residential real estate markets. According to James Dearsley and Professor Andrew Baum,

‘PropTech is one small part of the wider digital transformation of the property industry. It describes a movement driving a mentality change within the real estate industry and its consumers regarding technology-driven innovation in data assembly, transactions, and the design of buildings and cities.

The technology-driven innovation in the real estate sector includes, but is not limited to, the following:

Data analytical tools

Drones

Artificial intelligence

Internet of things

Blockchain

Smart contract

Financial technologies related to real estate

Smart homes, and

Virtual reality

These technologies are deployed in both the commercial and residential real estate markets. The market participants leverage the technology to create a more transparent market, less analog and improve real estate utilization. Fig 1 and Fig 2 provide pictorial explanations of the two market landscapes serviced by Proptech.

Fig 1: Commercial Proptech Landscape

Fig 2: Residential Proptech Landscape

3.0 WHY NOW (PROPTECH)?

Our world is currently experiencing a global digital revolution, Poptech is playing a crucial role in the revolution, creating a more efficient and sustainable service delivery to both homeowners and tenants.

The real estate sector is experiencing a late technology disruption compared to other industries, one of the major resistance to disruption is the uncertain feeling of homeowners adopting a new and unaccustomed means for the management of their most valuable asset. The world is changing and we have to adapt to modernization triggered by technology.

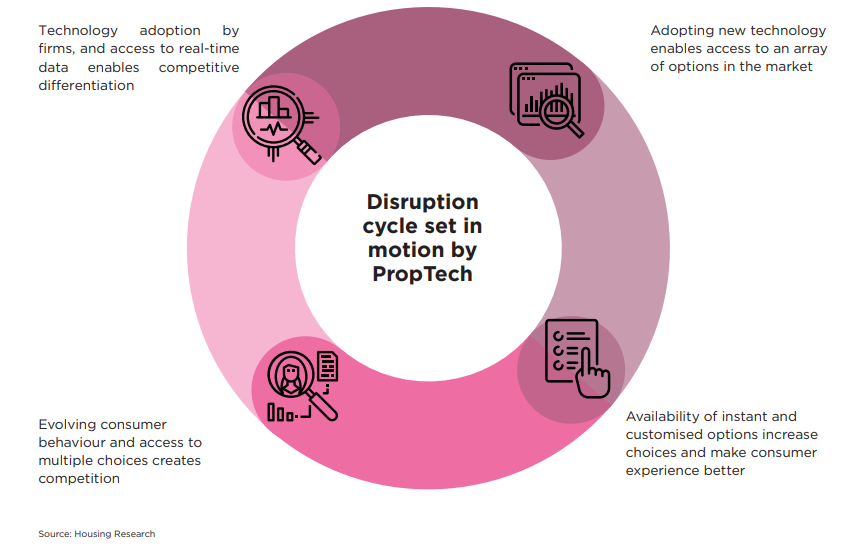

We can summarise the why now into 3 as shown in fig 3 below (see Proptech Global Trends 2021)

Fig 3: Why Now (Proptech)

4.0. THE IMPACT OF PROPTECH ON THE REAL ESTATE SECTOR

The commercial and residential Propetech market is expanding globally, and technology-driven solutions emergence is evolving, making available data and analytical insights to enable investors and real estate owners to make informed decisions concerning investment and operating decisions.

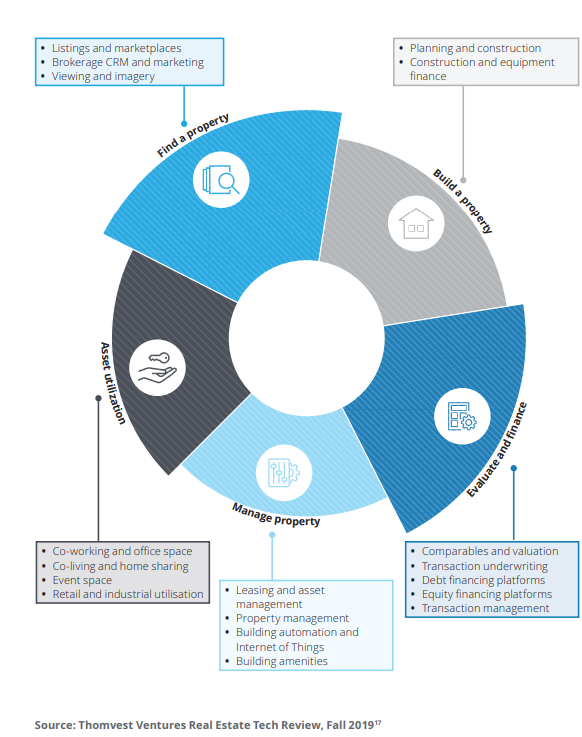

The real estate sector is evolving, affected by interconnected factors such as demographics, business structure, urbanization, consumer behavior, and globalization. With the adoption of technology, disruption in the sector has become more evident. As seen in the real estate value chain, there have been significant changes across the asset classes. Fig 4 gives a detailed view of the disruption cycle.

Fig 4: Disruption Cycle

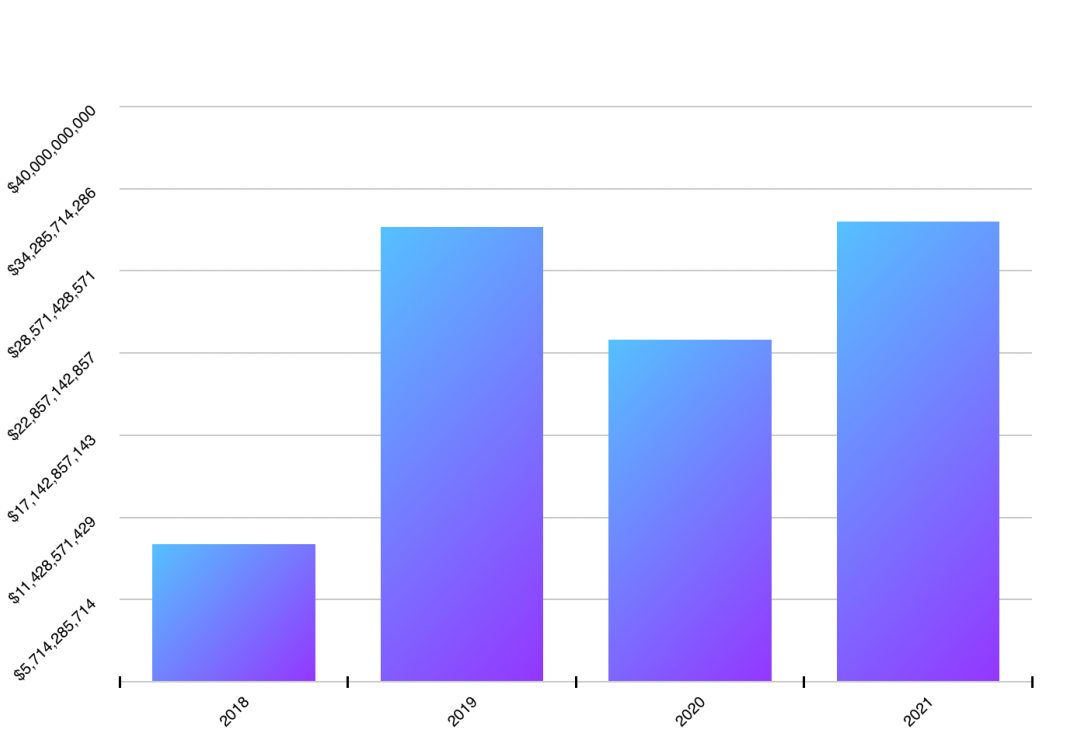

According to Deloitte's report, venture capital investment in real estate tech companies globally hit a record high of $31.5billion in 2019, an increase of 227% from 2018. The capital investment in the proptech space is increasing yearly with a projection of over $80billion by 2025. Fig 5 is a historical chart of investment in Proptech globally according to Real Estate Tech Venture Funding Report

Fig 5: Global Investment in Proptech from 2018-2021

The impact of proptech in the real estate sector can be summarized into three, based on the areas foreign investors find attractive:

Streamlined Efficiency: The adoption of the proptech solution embedded with big data analytics has eased evaluating the development, investment, leasing, buying, and selling process in the real estate sector. The real estate stakeholders can experience a more secure remote transaction and digital contracting, creating a faster and easier buying experience.

Cost-reduction: Technological advances have a great effect on shifting the supply curve to the right when such technology improves production efficiency. Adopting a Proptech solution embedded with automation tools aims at reducing the amount spent on unnecessary tasks, shrinking the chances of human error thereby creating efficiency in the delivery of services to potential clients.

Improved decision making: Adopting proptech solutions help in netting off “the middle man’’ who often has misaligned interests in property purchase and sales, affecting clients' decision-making. With Virtual Reality (a Proptech solution), home inspections, house tours, and viewing transition to the virtual world can be conducted by clients from the comfort of their homes, thereby improving their decision-making.

5.0. THE REAL ESTATE MARKET GAP IN NIGERIA

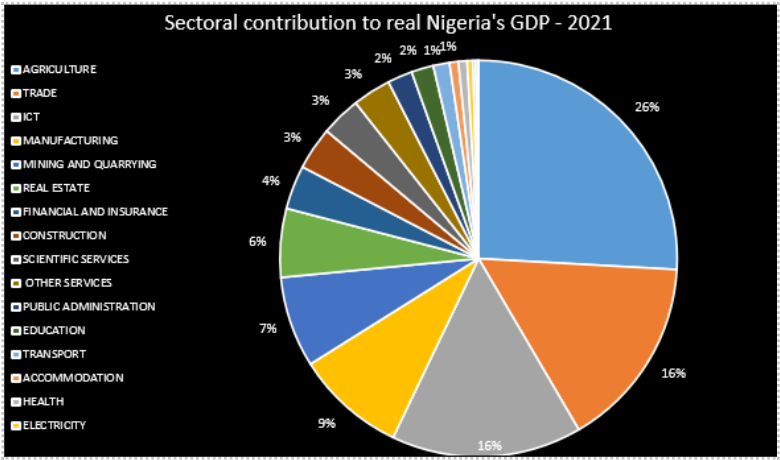

According to the GDP report of 2021 published by the National Bureau of Statistics, the real estate sector contributed a total of 5.28% to the real GDP, estimated at $5.3billion. Fig 6 shows that the real estate sector is one of the top 5 sector contributors to Nigeria’s GDP see Nairametrics report on GDP

Fig 6: GDP contributors (2021)

Consequently, on the viability of the sector, Mr. Gimba Ya’u Kumo (Former MD, Federal Mortgage Bank of Nigeria) posited that the value of the real estate market is about N59tn. He believed that the real estate sector is six times bigger than the local stock market, which is currently estimated at N12tn.

Mr. Gimba’s valuation was obtained from the market gap (serviceable market), which is based on the numeric value of the housing deficit we face in Nigeria, which is estimated to be 17million units which, when multiplied by the average cost of a single unit sums into N59tn.

In addition, if we run this same analysis using the population of Nigeria, which as of 2021 was estimated at a 211.4million. If we consider persons between the age of 30-45 will give us a market size of 34.67million people that can service the 17million housing deficit. This shows a huge potential for the real estate market, with huge revenues coming from solving the housing deficit and additional potential revenue from other related services. We can project over $2trillion from this market gap.

The serviceable available market of the commercial and residential business is huge and valued in trillions of naira. Our Nigerian real estate entrepreneurs have been unable to tap into 10% of this market. The advent of technology has impacted the growth of the market over time. We believe we can still have over 50% market share from the serviceable available market by leveraging more on technology and expanding its use in the real estate sector.

The sustainability of the real estate sector in Nigeria lies in how far we are ready to go to invest in technology platforms and solutions capable of connecting the demand area of housing need and supply area of the equation in closing the market gap. If technology adoption can push financial inclusion from 21.6% in 2010 to 64.1% in 2022, it is the best tool for closing the market gap in Nigeria.

To achieve sustainability, we must overcome the significant challenge facing the sector - Affordability - caused by the high cost of funds and production (construction). We all know the real estate sector requires enormous capital injection, and the cost of getting these funds tends to affect the affordability at the customer’s end. The advent of proptech is attracting foreign investors into the Nigerian real estate market; five proptech startups in Nigeria raised $ 2 million in 2021. The government needs to start creating policies to make the real estate sector more investor friendly.

6.0. USE CASES OF PROPTECH

The World Economic Forum classified the PropTech sector into three major categories:

PropTech 1.0: Growth of online listing sites back in 2007

PropTech 2.0: Use of data analytics and virtual reality to offer better and more specialized services for customers

PropTech 3.0: Experimentation with emerging technology such as drones, virtual reality tools, IoT, and Blockchain, which are trending currently.

Fig 7 below gives a detailed analysis of use cases of proptech to both developers and consumers.

Fig 7: Proptech Use Cases

Proptech solutions have been created for the following areas in the real estate sector;

Real Estate Search: This is the most common Proptech solution that has existed for a long time. With the evolution of Proptech, it gets better, and the core features the solution would have are;

Robust Geo-Mapping to convert salesforce list to a map

A range of search operators & filters to ease and provide precise information

Built-in graphs and charts to visualize search

Facility Management: This is a newly set up solution for the real estate sector, a more efficient means of monitoring properties virtually. The solution is powered by IoT and an extensive ecosystem of smart sensors that alert property owners of possible risks and ensure predictive maintenance. The core features the solution would have are;

Built-in maintenance planning modules to identify issues with your facility long before an issue arises

Built-in advanced management algorithms to offload piles of requests from tenants in order of urgency.

Construction Management: This is now getting popular within the housing development scheme in Lagos and Abuja, we are witnessing an uprising of smart homes, and total reliance on technology from the architectural stage to construction to furnishing of the houses (residential & commercial). Smart homes rely on construction management tools which help to make plans and create and keep documentation throughout the construction projects. The core feature the solution would have are;

Built-in project tracking tool to resolve any defects during construction via smartphone or tablet

Real-time communication channel with project stakeholders and client

Built-in CRM for sales after construction.

Investment Management (Fintech Real Estate): This is financial technology related to real estate, it involves the adoption of financial tools to provide financial services for the real estate sector. We are having this solution gradually increasing within our ecosystem, financial services with a focus on the real estate sector; investing, lending, purchasing, and rent payment.

Rental & Sales Tools: This is a proptech solution that aims at providing direct communication between tenants and property owners, making available house listings, and market overview.

The aforementioned solutions (uses cases) are the available option opened to the Nigerian real estate sector. Tech entrepreneurs and property owners adopting these solutions are going to be a game changer in the industry.

6.0. CONCLUSION

The real estate sector is evolving through the business model innovation and product innovation driven by the deployment of Proptech into the industry. We are now in an era where global technology entrepreneurs and investors are paying more attention to this evolution. Proptech is raising the bar in operational efficiency, customer engagement, innovation, and workforce productivity.

The evolution of proptech can be ascribed to a new digital reality disrupting the traditional business ecosystem. The embracement of technology structures such as; blockchain, alternative payment, BNPL, and AR&VR all create digital real estate ditching the traditional way of transacting in the real estate sector.

Proptech is the future, we can not overemphasize the relevance of technology in any given industry. The advancement of technology would greatly impact real estate areas such as; construction, marketing, sales, and rentals. Proptech would solve problems both homeowners and tenants experience regularly, the capabilities of technology are endless.

In Nigeria, with the recent rising of proptech, the real estate market will see more improvements in the coming years. The deployment of technology and apps will stir more movement within the industry. Proptech is the major tool for creating wealth in the real estate sector.

There are many opportunities to get involved with proptech, and the time is now!!!

7.0. REFERENCES

Property technology to disrupt Africa's real estate sector - Analysts

Powering digital transformation through proptech | PwC Canada

What is PropTech? (Importance, Startups and What/’s coming – Open Sourced Workplace

Nigeria's real estate market worth 59 Trillion Naira - FMBN Boss

What Is Proptech and How It Changed the Real Estate Industry

PropTech: Using technology to enhance real estate transparency, By Inyene Ibanga

Entrepreneur sees bigger prospects in the real estate market

What Is PropTech? +History, Startups, Trends in 2021 - 2ndKitchen

AT ANCHORIT INTERNATIONAL COMPANY

We help organizations start a journey of business and technology transformation to fast-track their way to success.

Anchorit International is a driven IT solutions company serving businesses in different industries across the globe. As a registered Software company, we do not just build IT solutions for businesses, we establish a long-lasting relationship that ensures the businesses we serve to grow to their full potential and profits.

Let us make your dream come true!!!

CONTACT ME

Egbetola Sola

(Product Counsel)

08138765200 (Whatsapp only)

ANCHORIT

solaegbetola@gmail.com